SME April 2026: Short-term revenue outlook deteriorates as rate pressure bites

Author: James Organ | Posted On: 11 May 2026

Updates to this research are published monthly.

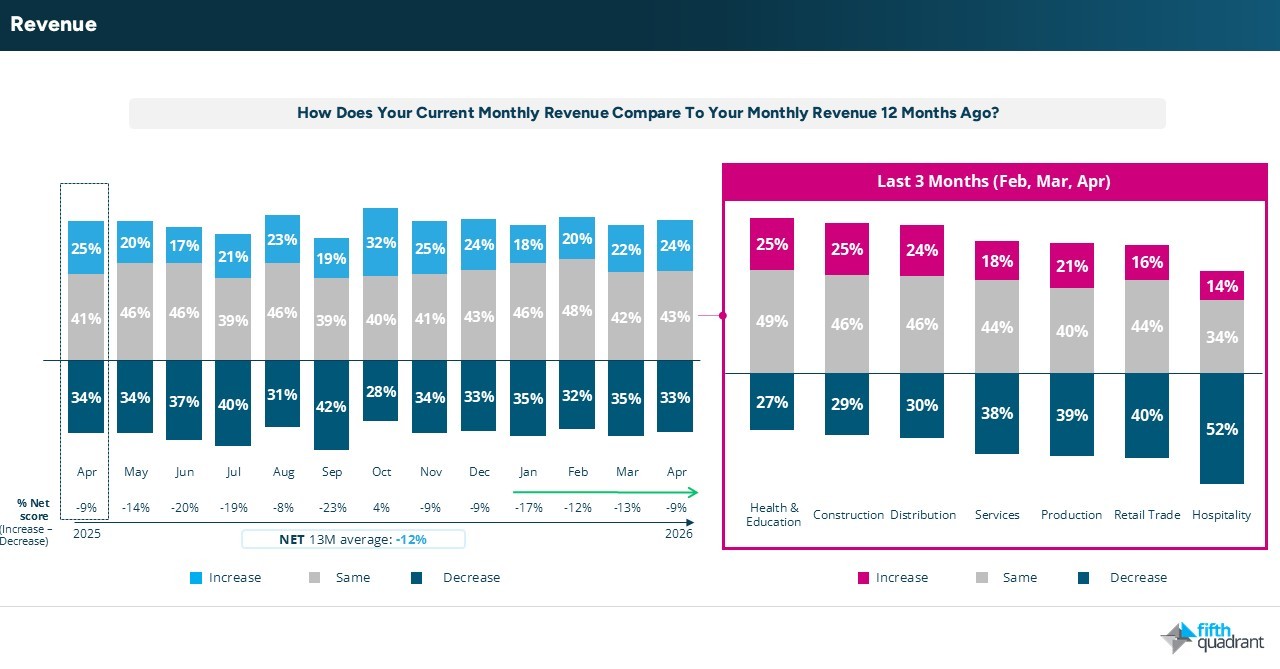

SME April 2026: Revenue has held broadly steady year-on-year (-9%), with a modest recovery emerging since early 2026 despite a volatile geopolitical and economic environment. April data shows signs of improvement, particularly in some sectors, although performance remains uneven, with hospitality continuing to lag and experiencing a difficult start to the year.

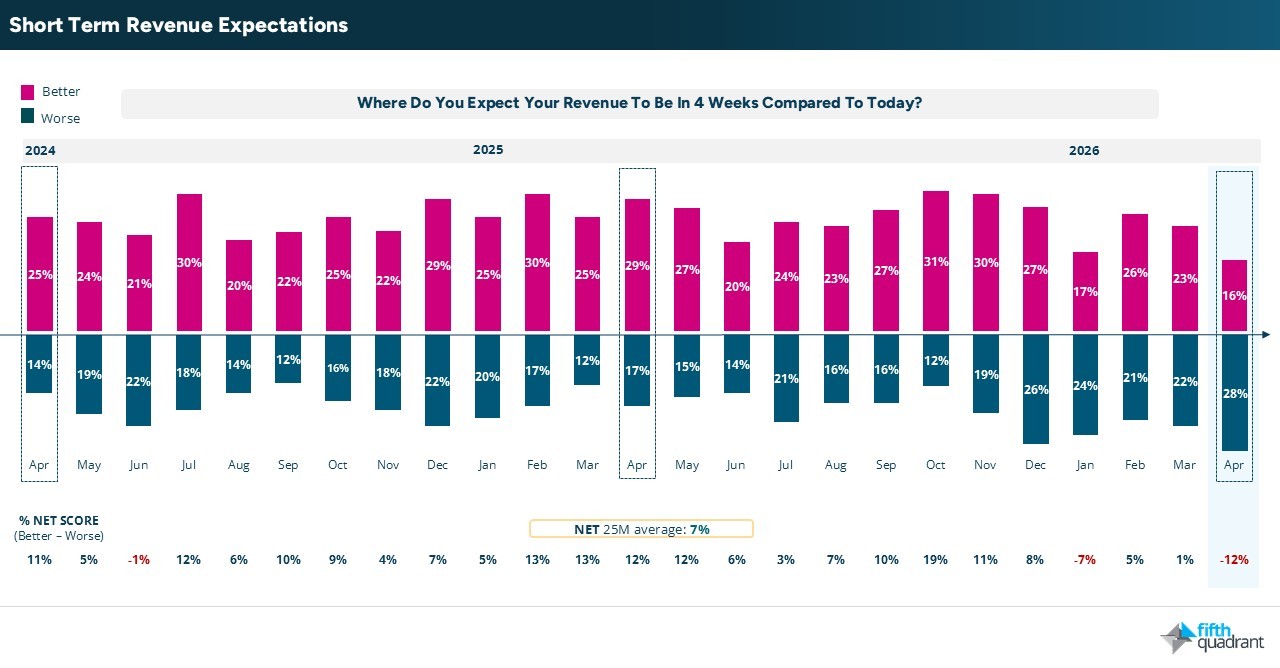

However, this improvement in current performance is not flowing through to expectations. Short-term revenue outlook has weakened significantly, with net expectations falling to their lowest level in the past two years. The April result represents a sharp decline from recent months and sits well below the longer-term average.

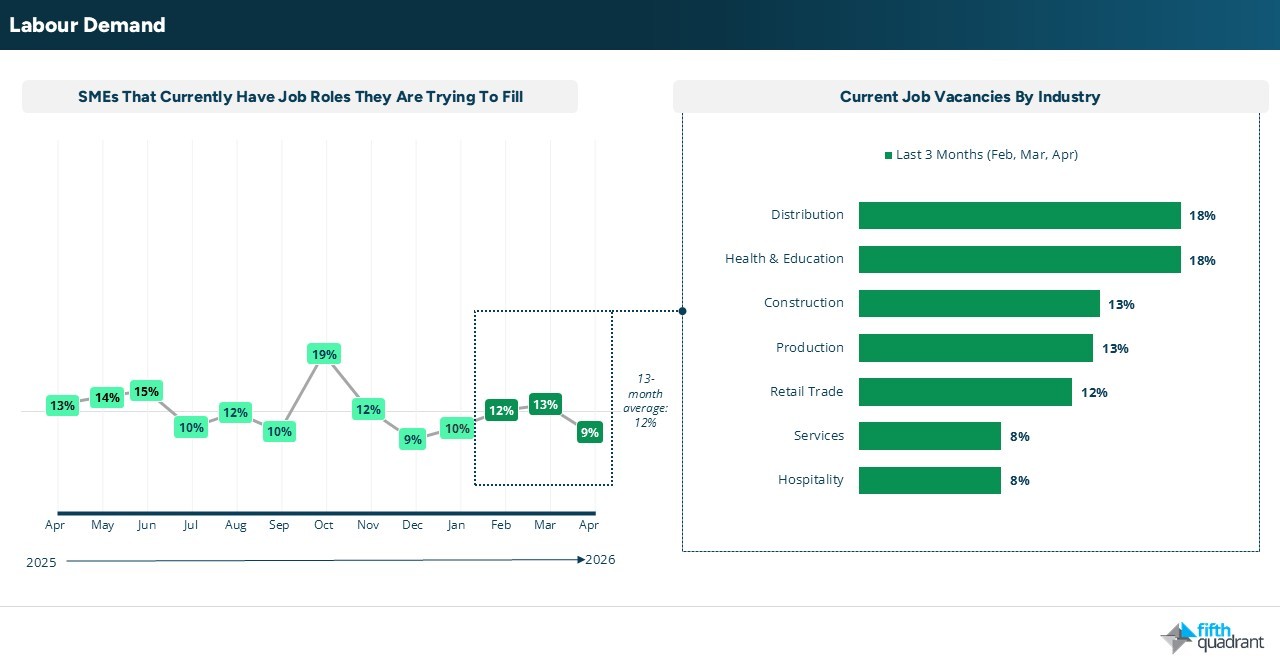

Labour market softens, but skills gaps persist

This disconnect between current performance and forward expectations reflects increasing external pressures. Ongoing geopolitical tensions, particularly the Iran conflict, alongside the confirmed RBA rate hike in May, are driving heightened uncertainty and weighing heavily on business confidence.

In response, businesses are maintaining a conservative operational stance. Hiring intentions remain subdued, with no meaningful recovery since late 2025. Job vacancies have declined to their lowest point over the past year, reinforcing weaker labour demand. Despite this, roles remain difficult to fill, pointing to ongoing skills mismatches and constrained labour mobility.

SMEs selectively deploy capital ahead of EOFY

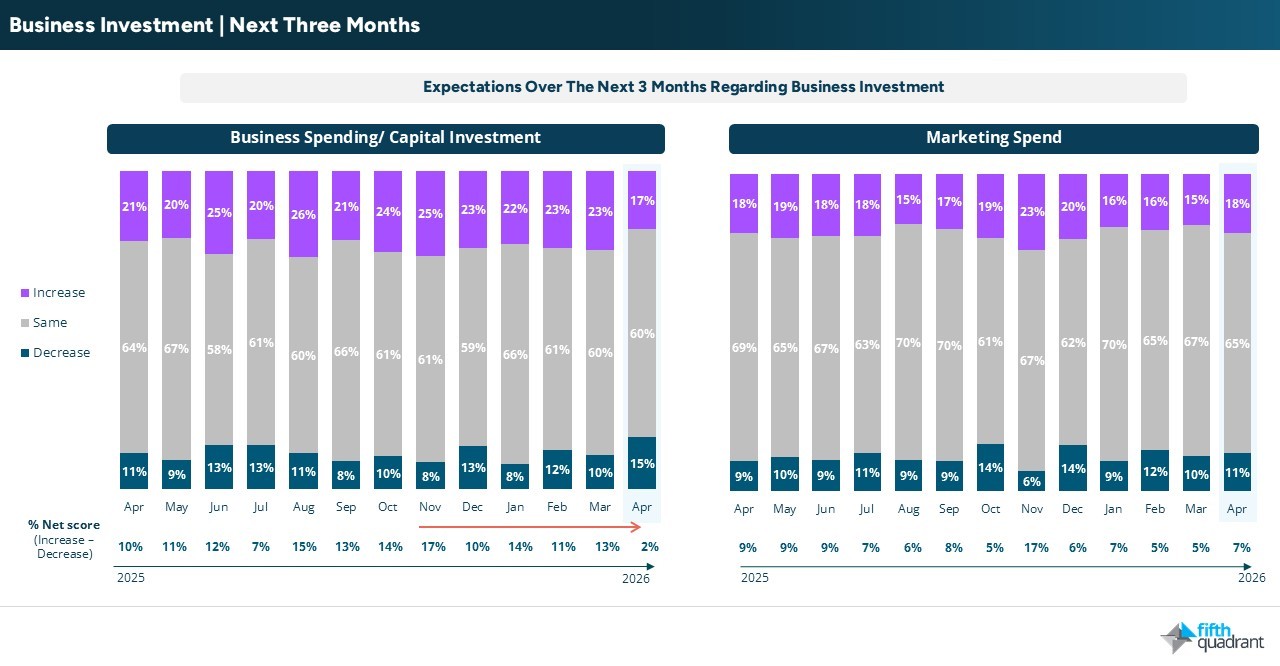

Capital expenditure intentions have continued to weaken from their November peak and remain well below April 2025 levels, while marketing spend has held relatively steady, indicating a focus on sustaining demand. At the same time, purchase intentions have increased across several asset categories, suggesting SMEs are selectively bringing forward spending to optimise tax outcomes ahead of EOFY.

Supporting this behaviour, demand for additional finance has risen from 9% to 13% in April, with a growing share of funds directed toward plant, machinery and equipment (29%). Importantly, this increase in borrowing has not translated into widespread financial stress, which remains contained at 7%.

Conclusion

With another interest rate hike, pressure on cashflow and demand is expected to intensify, pushing confidence lower. In response, SMEs continue to pull back on long-term commitments, tightly managing costs and labour, and selectively deploying capital, reinforcing a mindset focused on resilience.

Please click the link below to access the full report including subgroup analysis by industry sector, size of business and state. Fifth Quadrant and Ovation Research publish monthly updates of this SME market research here. For any questions or inquiries, feel free to contact us here.

SME December 2025

SMEs remain resilient

Posted in B2B, Consumer & Retail, Financial Services