SME February 2026: SME Growth Hits 12-Month Low

Author: James Organ | Posted On: 09 Mar 2026

Updates to this research are published monthly.

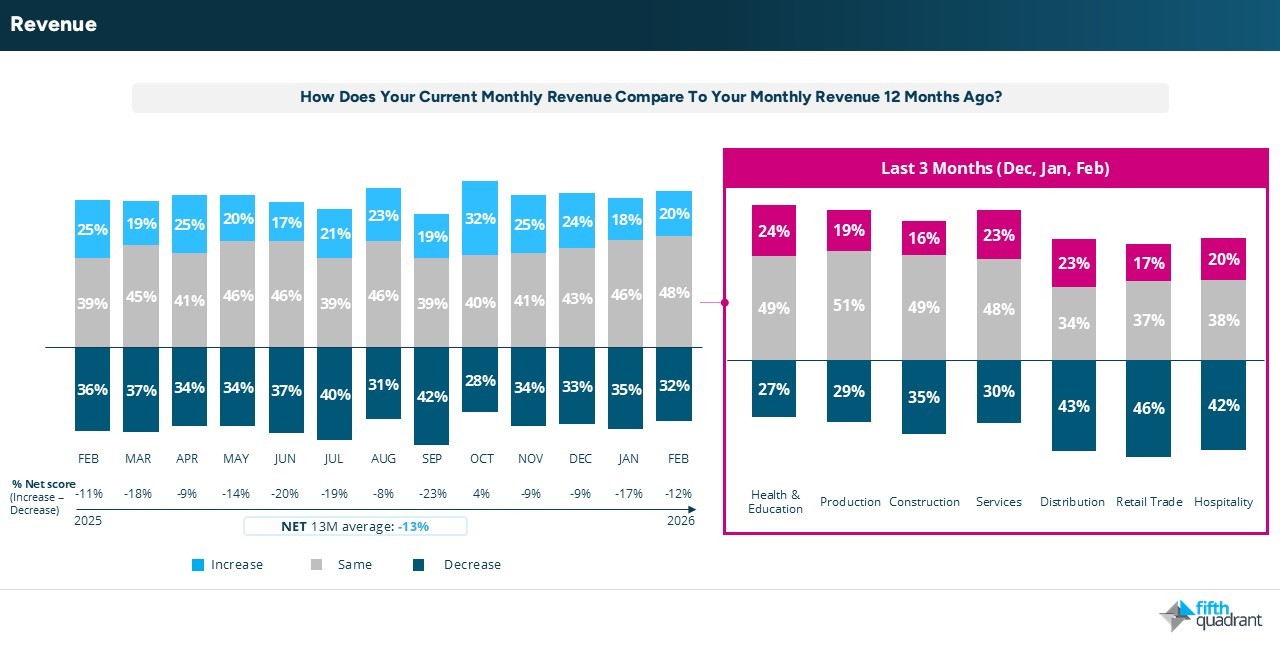

SME February 2026: SME revenues improved slightly in February, with the net score recovering to -12% from -17% in January, although still below levels recorded at the same time last year. Weakness continues to be broad-based, but particularly across Distribution, Retail Trade, and Hospitality.

Smaller businesses (0–19 employees) remain under pressure with a net score of -15%, while larger businesses (20+ employees) recorded a positive +17%.

Short-term revenue expectations also improved, with 26% of SMEs expecting higher revenues over the next four weeks, up from 17% in January. This rebound likely reflects seasonal demand following the holiday period, although expectations remain well below levels recorded in February over the past two years.

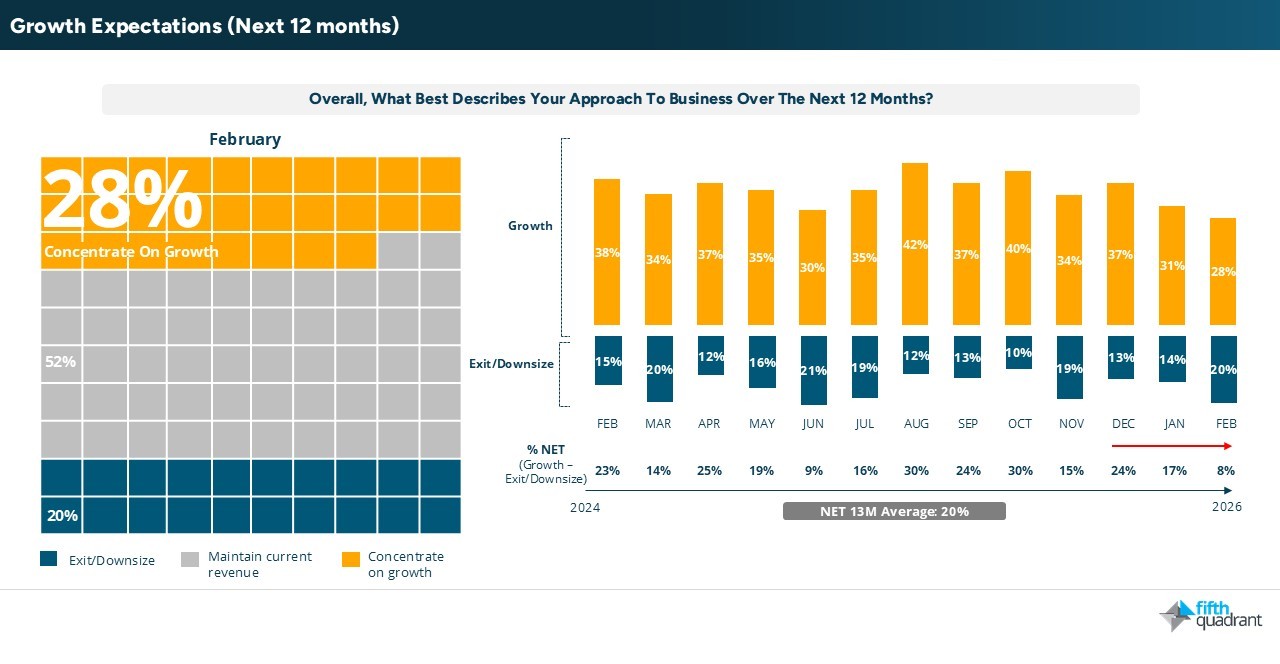

Growth Ambitions at Their Lowest Level in 12 Months

Despite the modest improvement in short-term revenue expectations, longer-term growth ambitions remain subdued. Only 28% of SMEs plan to prioritise growth over the next 12 months, the lowest level recorded in the past year. Hiring intentions also remain cautious, with 12% of SMEs reporting job vacancies, slightly below the 13-month average.

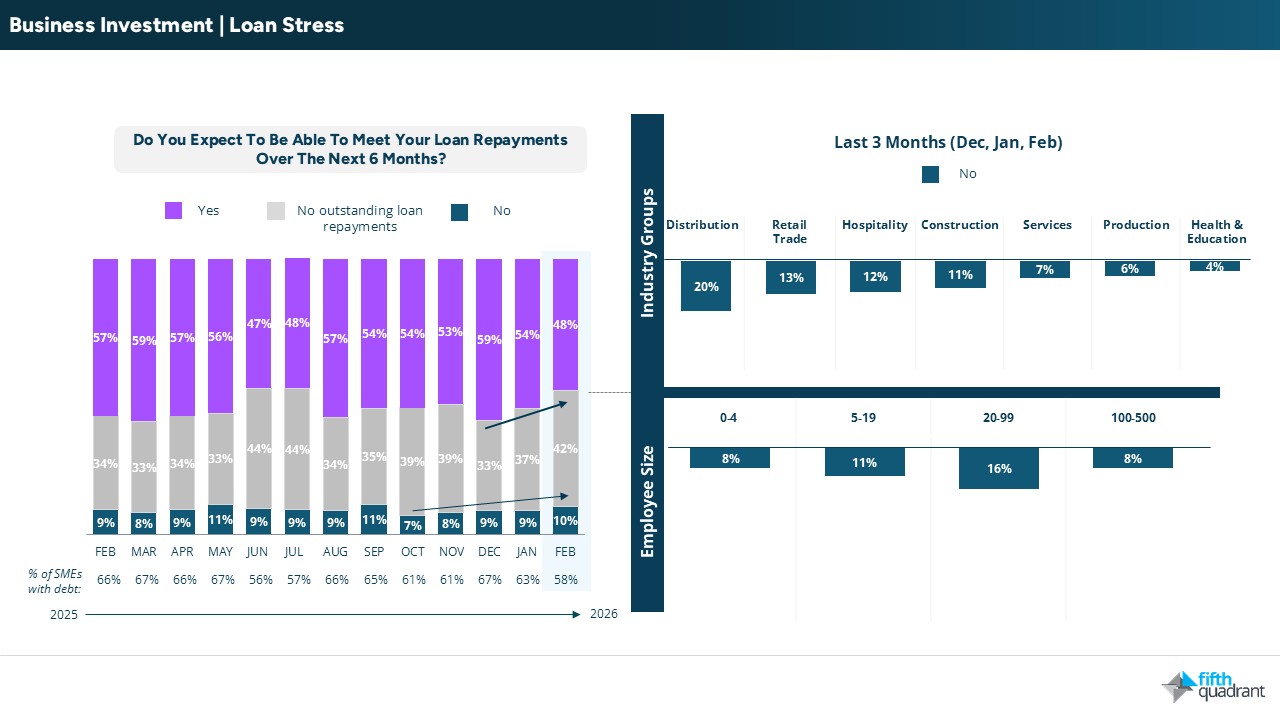

Loan Stress Edges Higher

Demand for additional finance has returned to the 13-month average, with funding primarily required to support cashflow and working capital rather than expansion. At the same time, demand for financing to support new market expansion and trade activity has declined, reflecting a more cautious approach to growth.

While the share of SMEs with outstanding debt fell to 58% in February, the lowest level since July, repayment pressures are increasing. The proportion expecting difficulty meeting loan repayments has risen from 7% in October to 10%, with pressures most evident among mid sized firms (20 to 99 employees), particularly in Distribution and Retail Trade.

Conclusion

In summary, February data reflects a mixed but broadly subdued picture for Australian SMEs. While revenue and short-term expectations have edged higher, profit has deteriorated and growth ambitions have reached a 12-month low. Businesses are responding to persistent cost pressures and economic uncertainty by prioritising efficiency and operational discipline over expansion, with the path to recovery remaining uncertain amid ongoing geopolitical and domestic headwinds.

Please click the link below to access the full report including subgroup analysis by industry sector, size of business and state. Fifth Quadrant and Ovation Research publish monthly updates of this SME market research here. For any questions or inquiries, feel free to contact us here.

SME December 2025

SMEs remain resilient

Posted in B2B, Consumer & Retail, Financial Services