Card Surcharges Are Ending. The Costs Aren’t

Author: James Organ | Posted On: 15 Apr 2026

What the RBA’s reform means for pricing, margins, and consumer behaviour.

The Reserve Bank of Australia’s decision to ban debit and credit card surcharges is being positioned as a win for consumers. It simplifies the experience. The price you see will be the price you pay. But beneath that simplicity sits a more significant shift. This change fundamentally reshapes how payment costs are distributed across the economy. For businesses, this is not just a compliance update. It is a pricing and margin reset.

For years, surcharges have operated as a direct cost recovery mechanism. They have allowed businesses to pass payment costs to the customers who generate them. A customer using a premium credit card pays more than one using debit or cash. The pricing signal is clear and immediate. That model is now being removed. In its place is an all-in pricing structure where payment costs are absorbed and spread across the entire customer base. The friction disappears at the point of sale, but the cost remains. It is simply embedded rather than itemised.

From explicit fees to embedded pricing

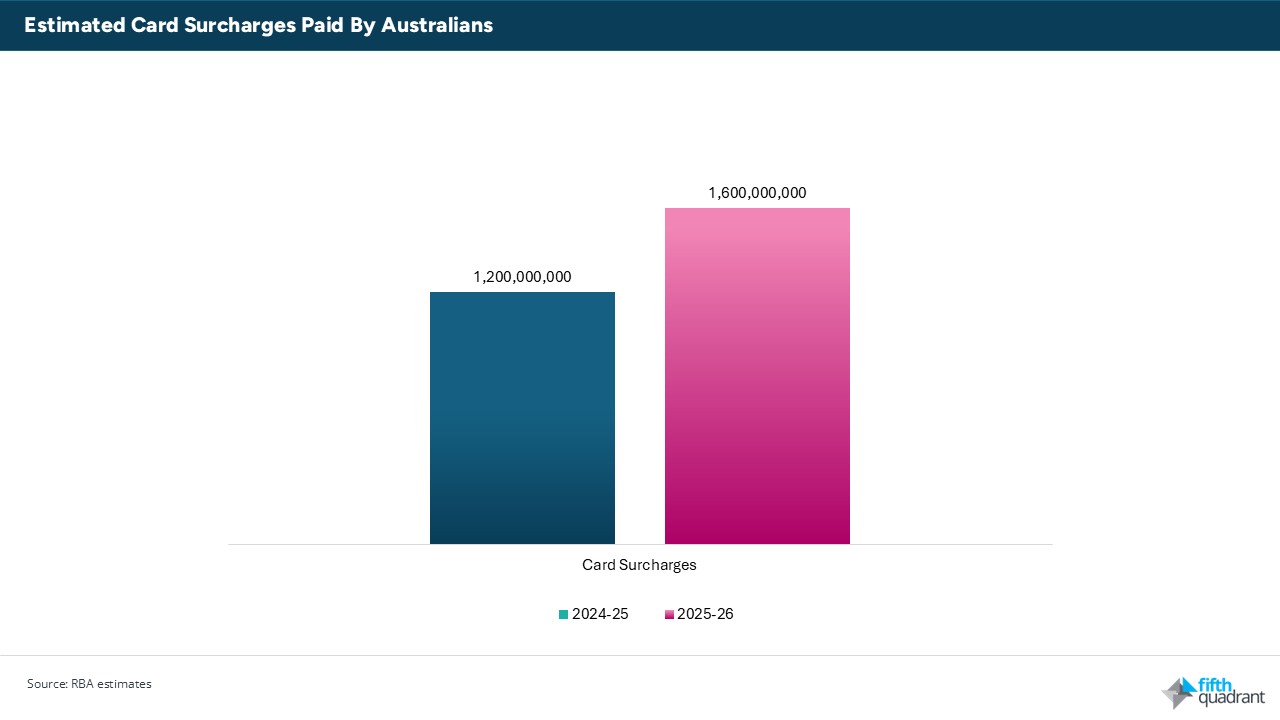

The scale of this shift is material. Australians are already paying more than $1 billion annually in surcharges, and that figure has grown meaningfully in recent years. The removal of surcharging does not eliminate this cost. It redistributes it. Prices will adjust, but incrementally. Instead of a visible surcharge applied at checkout, businesses will incorporate these costs into overall pricing. The result is a transition from explicit fees to implicit pricing, where all customers contribute regardless of how they pay.

This introduces a structural cross-subsidisation effect. Lower-cost payment users, including those paying by debit or cash, will contribute to the cost of higher-cost payment methods. At the same time, users of premium credit cards, particularly those benefiting from rewards programs, will capture more of the upside.

Margin pressure and strategic response

For businesses, particularly those operating on tighter margins, this changes the equation. Surcharging has been a simple and effective mechanism to protect margin. Without it, payment costs become another embedded expense that must be actively managed. Larger organisations may be able to offset this through scale, renegotiating terms with payment providers or optimising payment routing. Smaller businesses will have fewer levers available and may face greater pressure to absorb costs or adjust pricing more broadly.

The RBA’s changes to interchange fees add a further layer. By reducing the fees banks earn on card transactions, the regulator is lowering the system cost base. However, this will likely be offset elsewhere. Credit card rewards programs may become less generous, annual fees may increase, and the overall economics of card usage may shift over time.

At the same time, competitive pressure within the payments ecosystem will intensify. With surcharges removed, differentiation moves away from the checkout and into the underlying infrastructure. Lower-cost payment methods, including account-to-account and real-time payments, are likely to gain momentum as businesses look for ways to manage cost without direct price signalling.

For consumers, the experience improves. Pricing becomes clearer and more predictable. For businesses, the challenge becomes more complex. Payment costs are less visible, but no less material. This is ultimately a shift in how cost is communicated, not whether it exists. The experience becomes simpler. The economics do not.

Conclusion

For businesses, the opportunity is to respond deliberately. Those that actively manage pricing, payment mix, and cost recovery will be better positioned than those that simply absorb the change.

At Fifth Quadrant, we see this as part of a broader shift toward less visible but more embedded cost structures across markets. Understanding where those costs sit, and how they influence behaviour, will be critical for businesses over the next few years.

At Fifth Quadrant, we help organisations navigate shifts like the changes to Card Surcharges and the broader implications of RBA policy through deep market research and actionable insights. If you’re looking to understand how these reforms will impact your pricing, customers, and competitive position, get in touch with our team.

Posted in Uncategorized, B2B, Consumer & Retail