New vehicle sales February 2026: A softer market, but not for everyone

Author: Ben Selwyn | Posted On: 12 Mar 2026

New Vehicle Sales February 2026: 94,131 vehicles were sold in Australia in February 2026, down 2.7% on the same month last year. On the surface, a mild softening. Underneath it, a market dividing sharply between brands that are contracting and brands that are growing. The data points to a product story, and the brands most exposed are those with key models heading towards end of life.

Top takeaways

- Total market down 2.7% to 94,131 units in February, with the YTD deficit now at -1.3%.

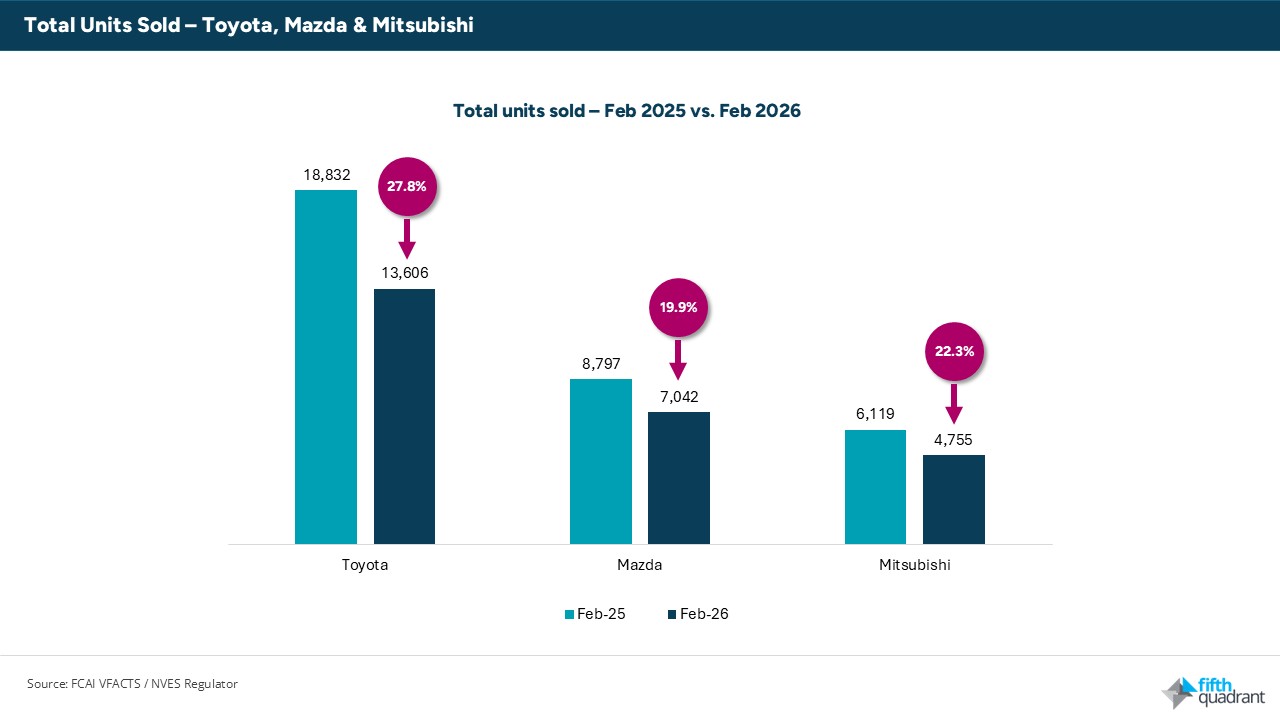

- Toyota fell 27.8%, Mazda fell 19.9%, Mitsubishi fell 22.3% together accounting for the majority of the headline decline.

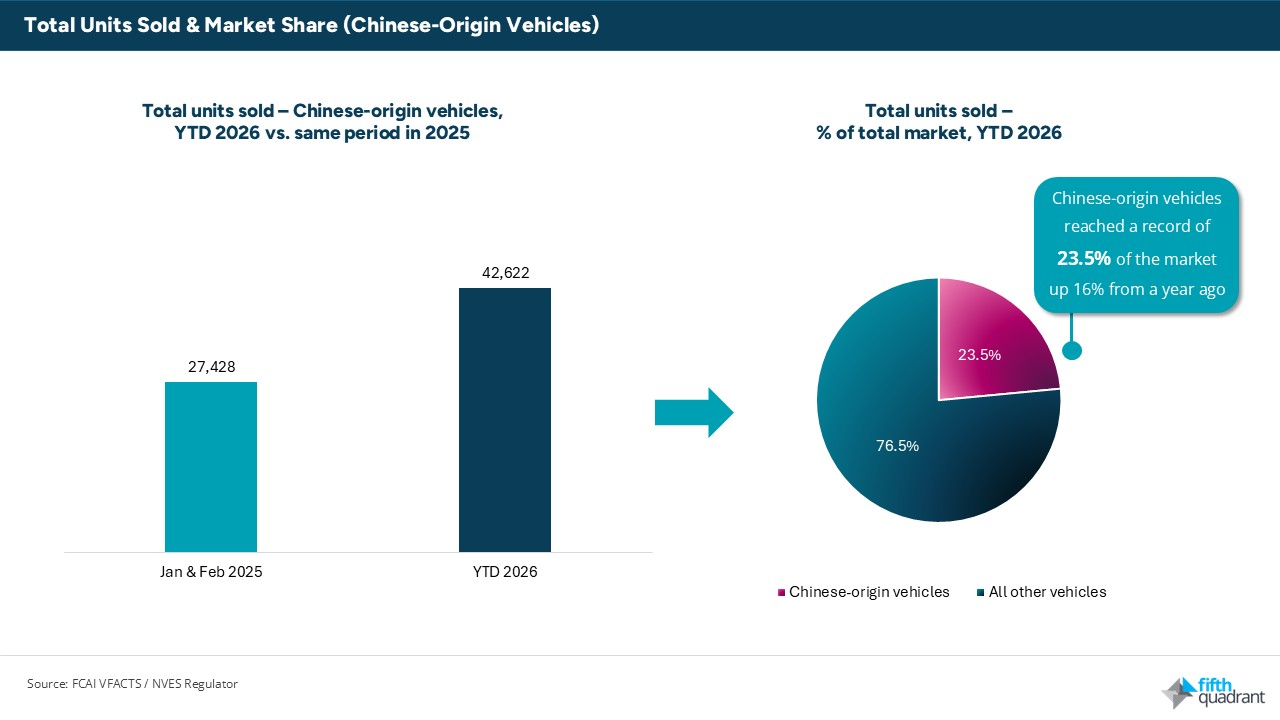

- Chinese-origin vehicles reached 22,362 units, a record 23.8% share of the market, up from around 16% a year ago.

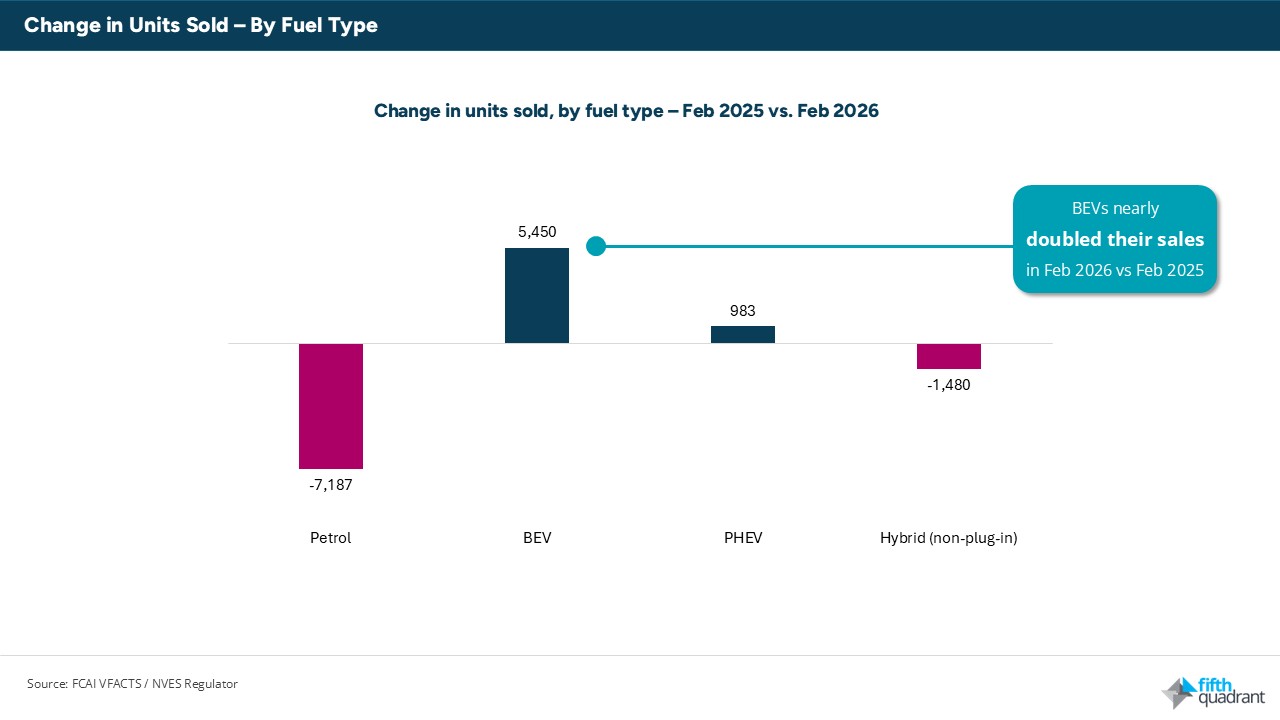

- BEVs reached 11,134 units for the month, nearly double February 2025. Petrol shed 7,187 units compared to the same month last year.

- PHEVs grew while hybrids declined in the SUV segment at least, buyers appear to be skipping the hybrid bridge and going straight to plug-in.

The product lifecycle is doing more damage than any macro trend

Three brands account for the bulk of February’s headline decline. Toyota sold 13,606 vehicles, down 27.8% on February 2025. Mazda sold 7,042, down 19.9%. Mitsubishi sold 4,755, down 22.3%. Together those three brands lost roughly 8,400 units compared to the prior year, in a market that declined by 2,579 overall. Without them, the market would have been close to flat.

At a model level, the Mitsubishi ASX fell 92.7% year-on-year, and the Eclipse Cross fell 97.7%. The Nissan Qashqai dropped 91.0%. These are not models losing ground to a better competitor, they are at or past the end of their Australian product cycles, and the volumes reflect it.

Toyota’s position is more nuanced. The Corolla held up reasonably well at 1,396 units, and the brand’s commercial lineup continues to perform. But the RAV4, which sold 5,076 units in a single month a year ago, is constrained by supply transition as the new generation comes through. That one model, at its prior run rate, would have more than offset the entire market decline on its own.

The contrast with recently refreshed or newly launched models is direct. The Tesla Model Y sold 2,791 units after its mid-cycle refresh, more than double its February 2025 result of 1,357. The Hyundai Tucson, updated for the current cycle, was up 15.8% to 1,705 units. The Isuzu MU-X, refreshed in 2025, grew 81.2% to 1,292 units. The BYD Sealion 7, launched in late 2024, sold 1,327 units having barely registered 12 months earlier. The Chery Tiggo 7 Pro, also recently introduced, sold 827 units against a base of 236 a year ago.

The market is not short of demand. It is short of new product in key segments from some of the brands that have historically set the standard.

Chinese brands reach a new record share

Chinese-origin vehicles accounted for 22,362 units in February, representing 23.8% of the total market. That is a new monthly record, ahead of the 21.4% share recorded in January. The year-to-date figure now sits at 23.5%, with 42,622 Chinese-origin vehicles sold in the first two months of 2026 compared to 27,428 in the same period last year.

BYD continues to lead the charge. At 5,323 units, BYD ranked fourth overall for the month, behind only Toyota, Mazda and Hyundai. The Sealion 7 was its top-selling model at 1,327 units, but what stands out is the breadth of the lineup. The Shark 6 ute contributed 1,058 units, making BYD a genuine light commercial player alongside its passenger and SUV presence. The Sealion 8, recently introduced, added 479 units. BYD now has volume across nine distinct models.

GWM followed with 4,689 units (up 24.9%), and Chery reached 3,938 (up 93.2%), driven largely by the Tiggo 7 Pro. New entrant Geely registered 893 SUV units with no comparable prior-year figure. Zeekr is also appearing in the data, with 9 units in February representing early-stage distribution rather than volume, but confirming that the pipeline of Chinese entrants is not yet closed.

MG is the exception that qualifies the trend. At 3,254 units, MG declined 13% year-on-year. The MG ZS, once a top 10 model, sold 1,337 units against 1,720 a year ago. The Chinese market is not uniformly growing. MG is a case in point, losing ground to newer Chinese entrants rather than to the established Japanese and European players it was displacing 12 months ago.

Petrol’s decline accelerates, and the hybrid bridge is shortening

Petrol-powered vehicles shed 7,187 units compared to February 2025, falling from 40,496 to 33,309. That follows a similar-scale decline in January, suggesting that this is a structural shift rather than month-to-month noise.

BEVs reached 11,134 units for the month, up from 5,684 in February 2025, largely driven by SUVs which jumped from 3,949 to 8,835 units in a single year. PHEVs also grew, reaching 5,854 units against 4,871 a year ago.

The more interesting signal is what hybrids did in the same period. Despite being the conventional stepping stone toward electrification, non-plug-in hybrids declined by 1,480 units in the month. In the SUV segment specifically, buyers appear to be moving to BEV and PHEV directly rather than treating the hybrid as a necessary intermediate step. If that pattern holds, the assumptions built into many dealer and fleet planning models around hybrid demand will need revisiting.

The rental channel is also worth tracking. Rental purchases reached 5,786 units in February, up 1,513 on the prior year. Rental fleets are where new powertrains get trialled at scale before fleet managers commit to broader adoption. If Chinese BEVs and PHEVs are entering the rental pool in volume, that exposure will feed through to consumer consideration in ways that won’t show up in brand tracking surveys for another 6 to 12 months.

What February tells us about 2026

February’s numbers continue the trends we saw in the January data. The market’s modest YTD decline is almost entirely explained by a handful of brands with ageing product cycles. The structural powertrain shift is accelerating regardless of overall volume. And Chinese brands look like they’ll be pushing their Japanese competition for overall market leadership at the end of 2026.

Fifth Quadrant publish monthly new vehicle sales updates here. For more insights on automotive market trends and consumer behaviour, explore Fifth Quadrant’s automotive market research reports or contact our team.

FCAI VFACTS, Electric Vehicle Council Vehicle Sales Report. Analysis by Fifth Quadrant.

Posted in Auto & Mobility, B2B, Uncategorized